A letter from Tom Standage, editor of “The World Ahead 2023”

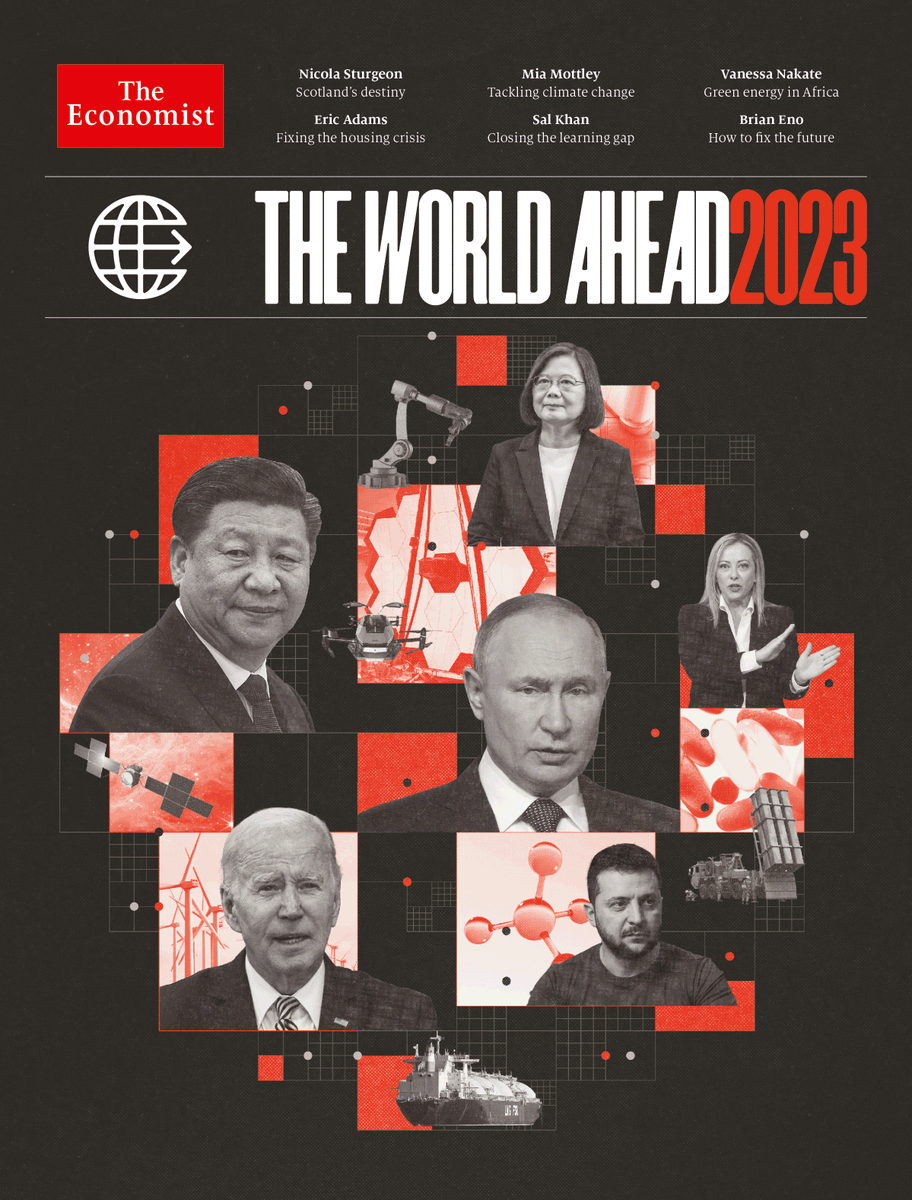

1. All eyes on Ukraine. Energy prices, inflation, interest rates, economic growth, food shortages—all depend on how the conflict plays out in the coming months. Rapid progress by Ukraine could threaten Vladimir Putin, but a grinding stalemate seems the most likely outcome. Russia will try to string out the conflict in the hope that energy shortages, and political shifts in America, will undermine Western support for Ukraine.

2. Recessions loom. Major economies will go into recession as central banks raise interest rates to stifle inflation, an after-effect of the pandemic since inflamed by high energy prices. America’s recession should be relatively mild; Europe’s will be more brutal. The pain will be global as the strong dollar hurts poor countries already hit by soaring food prices.

3. Climate silver lining. As countries rush to secure their energy supplies, they are turning back to dirty fossil fuels. But in the medium term the war will accelerate the switch to renewables as a safer alternative to hydrocarbons supplied by autocrats. As well as wind and solar, nuclear and hydrogen will benefit too.

4. Peak China? Some time in April China’s population will be overtaken by India’s, at around 1.43bn. With China’s population in decline, and its economy facing headwinds, expect much discussion of whether China has peaked. Slower growth means its economy may never overtake America’s in size.

5. Divided America. Although Republicans did worse than expected in the midterm elections, social and cultural divides on abortion, guns and other hot-button issues continue to widen after a string of contentious Supreme Court rulings. Donald Trump’s formal entry into the 2024 presidential race will pour fuel on the fire.

6. Flashpoints to watch. The intense focus on the war in Ukraine heightens the risk of conflict elsewhere. With Russia distracted, conflicts are breaking out in its backyard. China may decide that there will never be a better time to make a move on Taiwan. India-China tensions could flare in the Himalayas. And might Turkey try to nab a Greek island in the Aegean?

7. Shifting alliances. Amid geopolitical shifts, alliances are responding. nato, revitalised by the war in Ukraine, will welcome two new members. Will Saudi Arabia join the Abraham accords, an emerging bloc? Other groupings of growing importance include the Quad and aukus (two American-led clubs intended to deal with China’s rise) and i2u2—not a rock band, but a sustainability forum linking India, Israel, the United Arab Emirates and the United States.

8. Revenge tourism. Take that, covid! As travellers engage in post-lockdown “revenge” tourism, traveller spending will almost regain its 2019 level of $1.4trn, but only because inflation has pushed up prices. The actual number of international tourist trips, at 1.6bn, will still be below the pre-pandemic level of 1.8bn in 2019. Business travel will remain weak as firms cut costs.

9. Metaverse reality check. Will the idea of working and playing in virtual worlds catch on beyond video games? 2023 will provide some answers as Apple launches its first headset and Meta decides whether to change its strategy as its share price languishes. Meanwhile, a less complicated and more immediately useful shift may be the rise of “passkeys” to replace passwords.

10. New year, new jargon. Never heard of a passkey? Fear not! Turn to our special section, “Understand This”, which rounds up the vital vocabulary that will be useful to know in 2023. nimbys are out and yimbys are in; cryptocurrencies are uncool and post-quantum cryptography is hot; but can you define a frozen conflict, or synfuel? We’ve got you covered.

A selection of three essential articles read aloud from the latest issue of The Economist. This week, the coming house-price slump, why Xi Jinping has no interest in succession planning (10:10) and how to make better use of antidepressants (19:29).

A country of political instability, low growth and subordination to the bond markets

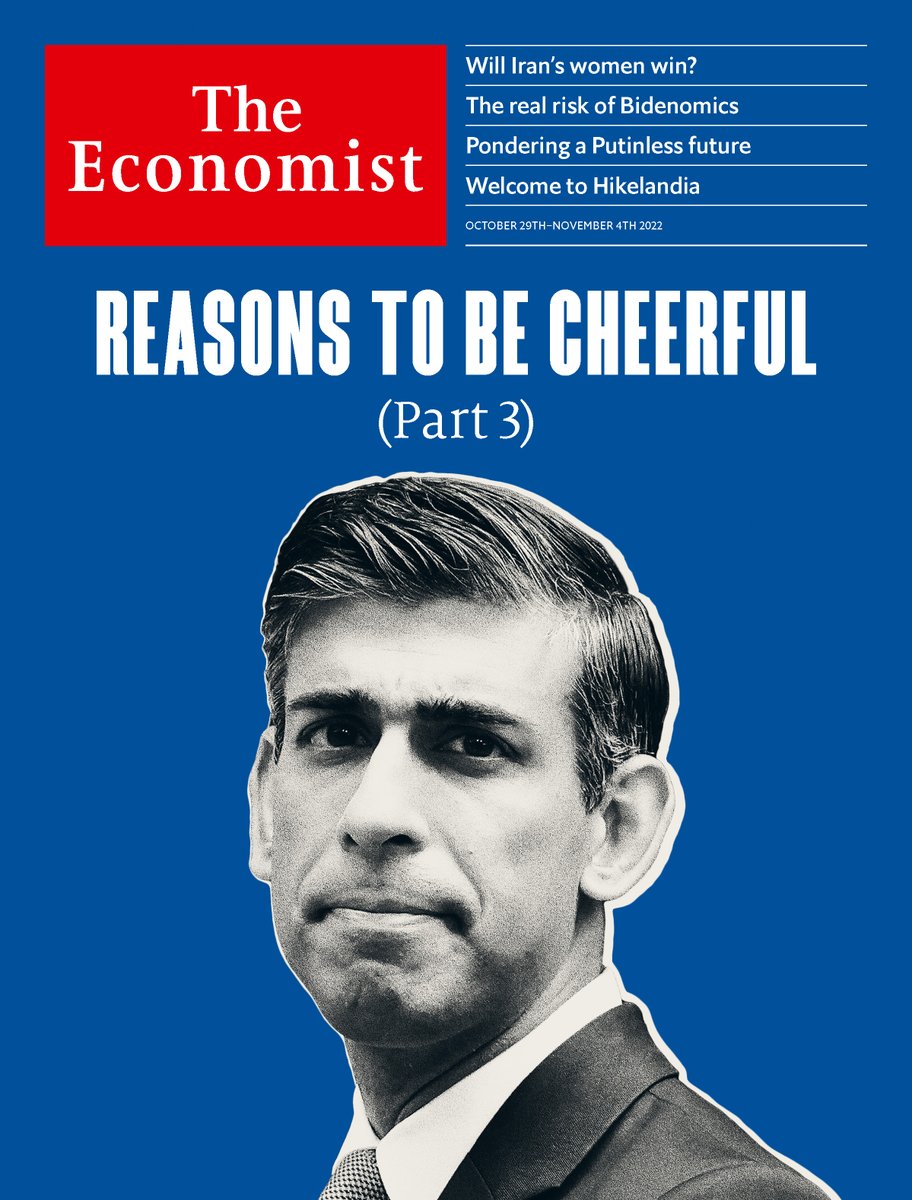

In 2012 liz truss and Kwasi Kwarteng, two of the authors of a pamphlet called “Britannia Unchained”, used Italy as a warning. Bloated public services, low growth, poor productivity: the problems of Italy and other southern European countries were also present in Britain. Ten years later, in their botched attempt to forge a different path, Ms Truss and Mr Kwarteng have helped make the comparison inescapable. Britain is still blighted by disappointing growth and regional inequality. But it is also hobbled by chronic political instability and under the thumb of the bond markets. Welcome to Britaly.

A selection of three essential articles read aloud from the latest issue of The Economist. This week, the outlook for the world economy, how worried you should be about Elon Musk’s superpowers (12:50), and a study allays fears that covid vaccines harm menstrual cycles (16:50).

The new prime minister must eschew pantomime radicalism if she is to succeed. The sceptics have many reasons to be dubious—yet underestimating Liz Truss is a mistake her opponents have already made to their cost.

A selection of three essential articles read aloud from the latest issue of The Economist. This week, the disunited states of America, why Britain can’t build (9:15) and Pakistan’s worst floods in recent memory (17:05).

Two states, two very different states of mind. On August 25th California banned the sale of petrol-powered cars from 2035, a move that will reshape the car industry, reduce carbon emissions and strain the state’s electricity grid. On the same day in Texas a “trigger” law banned abortion from the moment of conception, without exceptions for rape or incest. Those who perform abortions face up to 99 years in prison.

News, Views and Reviews For The Intellectually Curious