In the new series “Economics For People” from the Institute for New Economic Thinking (INET), University of Cambridge economist and bestselling author Ha-Joon Chang explains key concepts in economics, empowering anyone to hold their government, society, and economy accountable.

In the new series “Economics For People” from the Institute for New Economic Thinking (INET), University of Cambridge economist and bestselling author Ha-Joon Chang explains key concepts in economics, empowering anyone to hold their government, society, and economy accountable.

Lecture 1.1: The Nature of Economics

Lecture 1.2: Five Reasons Why Economics Is Political

Lecture 2: What Is Wrong With Globalization?

To view more videos: https://www.ineteconomics.org/perspectives/videos/economics-for-people

Paul Volcker, who

Paul Volcker, who

Shoppers have to use a debit card at the door to gain entry to the store. Then they can shop for products and just walk out. Upon exit, customers can verify their purchases against the receipt. No cash is accepted.

Shoppers have to use a debit card at the door to gain entry to the store. Then they can shop for products and just walk out. Upon exit, customers can verify their purchases against the receipt. No cash is accepted.

Wall Street Journal corporate bureau chief Marcelo Prince explains the competition between retailers Amazon, Target and Walmart to provide one-day shipping to customers during the holiday season.

Wall Street Journal corporate bureau chief Marcelo Prince explains the competition between retailers Amazon, Target and Walmart to provide one-day shipping to customers during the holiday season.

As digital payments become the norm, will there be a need for cash? The Economist’s Finance editor Helen Joyce takes a look behind the scenes of the future, from Sweden to Shanghai. She explores how digital payments will transform the economy, and how they risk leaving some people behind.

As digital payments become the norm, will there be a need for cash? The Economist’s Finance editor Helen Joyce takes a look behind the scenes of the future, from Sweden to Shanghai. She explores how digital payments will transform the economy, and how they risk leaving some people behind.

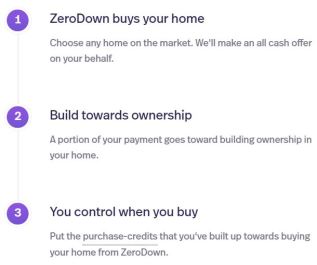

Real estate startup ZeroDown, which launched earlier this year, boasts a unique business model. Aiming to help more people become homeowners in the pricey San Francisco Bay Area, the company removes several of the largest hurdles from the homebuying process, namely the down payment and mortgage, and buys homes for its customers outright.

Real estate startup ZeroDown, which launched earlier this year, boasts a unique business model. Aiming to help more people become homeowners in the pricey San Francisco Bay Area, the company removes several of the largest hurdles from the homebuying process, namely the down payment and mortgage, and buys homes for its customers outright.

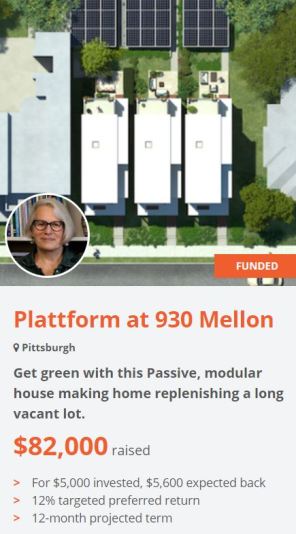

Small Change raised $82,000 in equity to help construct

Small Change raised $82,000 in equity to help construct