BARRON’S MAGAZINE (December 28, 2024): The latest issue features ‘The Real Drone Invasion’….

Watch Out, Amazon and UPS: The Race Is On for Drone Delivery

There’s more to drones than mysterious lights. A multibillion-dollar drone delivery market is taking shape. The rewards could be massive.

UnitedHealth and CVS Received Millions in Opioid Rebates Through Medicare

As the U.S. opioid crisis deepened, Medicare plans administered by UnitedHealth and CVS Health were a top source of OxyContin sales, a Barron’s investigation found.

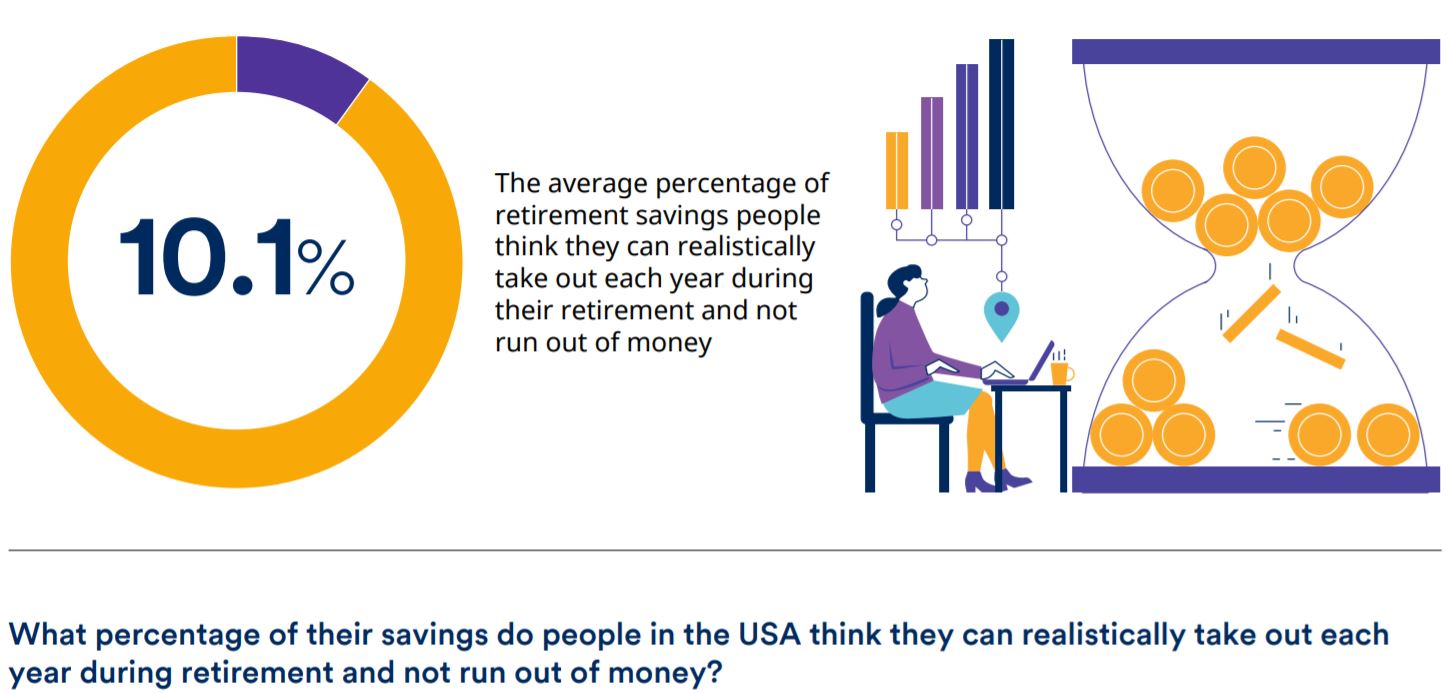

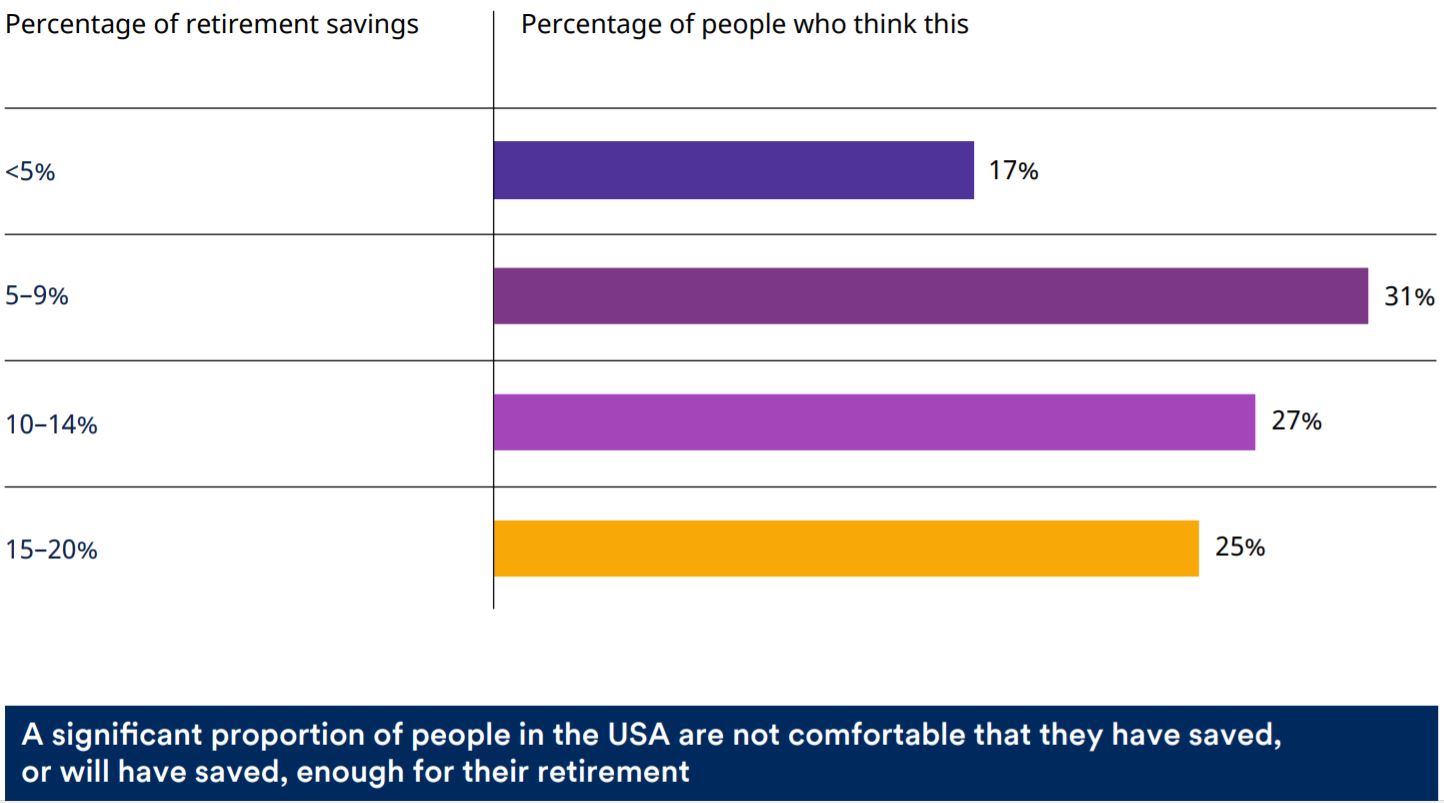

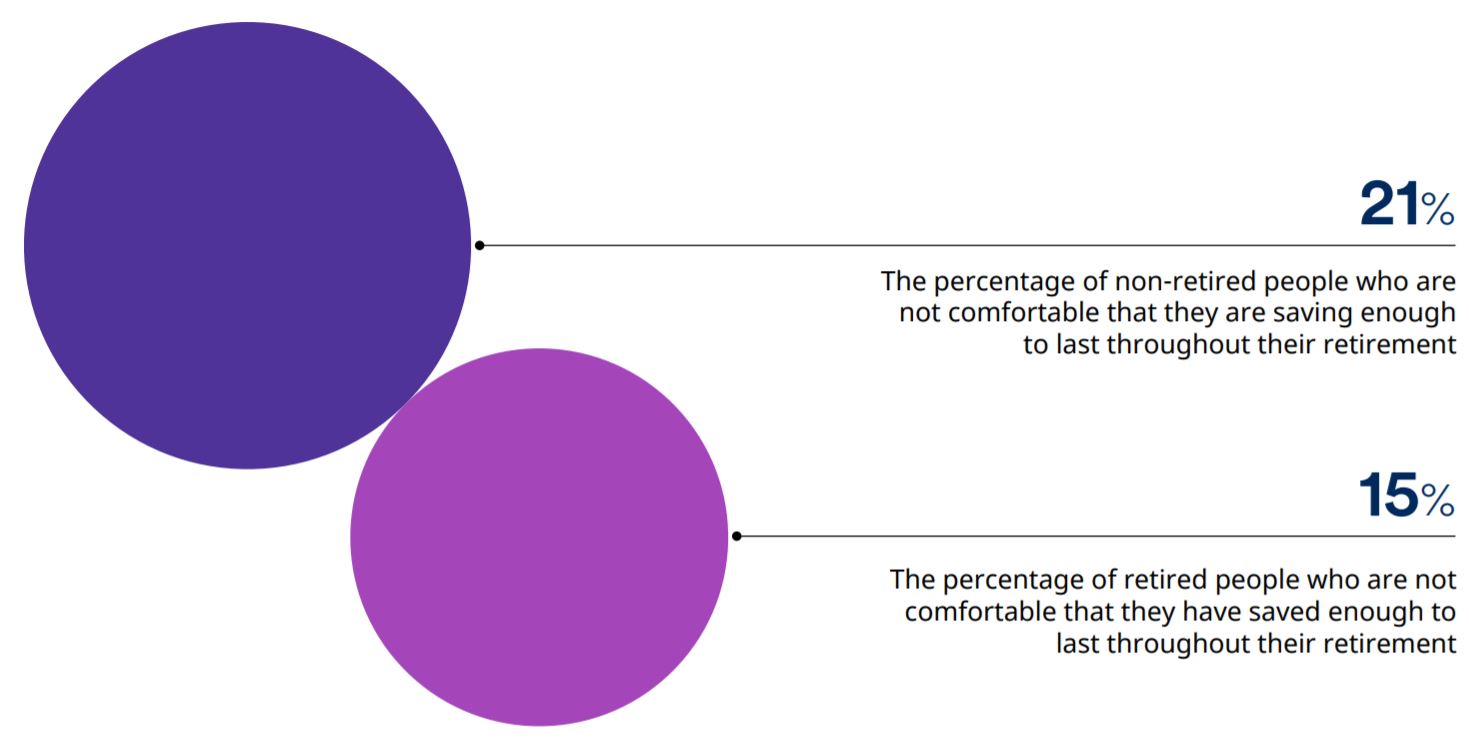

Welcome to Middle Age, Millennials. Here’s How to Get Your Retirement Savings on Track.

AI Is Reshuffling the Ranks of Utilities Stocks. Here Are the Likely Winners.

Once known as safety plays, shares of electricity suppliers are getting a jolt from AI data centers.