A.M. Edition for May 14. WSJ’s Rochelle Toplensky discusses Internal Revenue Service attention on cryptocurrency investors. WSJ’s Betsy McKay on the continuing search for clues about the origin of the Covid-19 pandemic.

And, air travelers face new frustrations. Marc Stewart hosts.

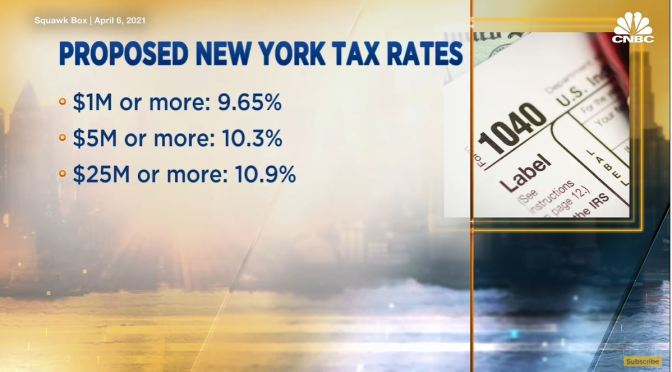

To balance their budgets during the coronavirus pandemic, states including New Jersey and New York have raised taxes on the wealthy. Conservatives warn that it will cause many of those who left at the onset of the pandemic make those moves permanent since they’re no longer bound to the physical locations of their offices or their children’s schools. But available data from 2020 show that the so-called exodus wasn’t as pronounced as initially projected, and the urban exit that did happen, was to suburbs rather than low tax states.

Five stories to know for April 23: Biden hosts climate change summit, Senate passes bill to fight anti-Asian hate crimes, Daunte Wright funeral, Biden’s tax plan and India’s COVID surge.

1. The United States and other countries hiked their targets for slashing greenhouse gas emissions at a global climate change summit hosted by President Joe Biden, an event meant to resurrect U.S. leadership in the fight against global warming.

2. A hate crimes bill to combat violence against Asian Americans in the wake of the COVID-19 pandemic passed the Senate overwhelmingly, a rare bipartisan vote in the evenly divided chamber. The bill passed 94-1, with Missouri Senator Josh Hawley the only no vote. It must pass the House of Representatives, where Democrats hold a clear majority. President Joe Biden has called for passage.

3. Hundreds of mourners filled a Minneapolis church for the funeral of Daunte Wright.

4. Biden will roll out a plan to raise taxes on the wealthiest Americans, including the largest-ever increase in levies on investment gains, sources say.

5. A police convoy escorting a tanker carrying oxygen reached a hospital in India’s capital just in time, to the huge relief of doctors and relatives of COVID-19 patients counting on the supply. India reported the world’s highest daily tally of coronavirus infections for a second day on Friday, surpassing 330,000 new cases, as it struggles with a health system overwhelmed by patients and plagued by accidents.

The coronavirus pandemic disrupted the global economy in ways that may affect your 2020 taxes. WSJ tax reporter Richard Rubin shares his tips for this unusual tax season. Photo illustration:Laura Kammermann

Social Security benefits are federally taxed at three different tiers. The amounts depend on your income, marriage status and whether you file jointly or separately. Paying less in taxes can come down to how much money you pull out of your retirement accounts in a given year. Watch this video for tips on how to pay less in taxes on your Social Security benefits.

Tesla’s gigafactory and Apple’s second-largest campus aren’t the only big businesses coming to Texas. From Oracle to Hewlett Packard Enterprise, Elon Musk to Joe Rogan, Texas has lured an increasing number of big businesses and billionaires away from California since the pandemic began. While California’s population and job growth both slowed to a trickle, Texas added more residents than any other state in 2020. CNBC talks to those moving and longtime Texans about the reasons behind the trend and what it could mean for the future of the Lone Star State.

As Oracle, Palantir and Hewlett-Packard Enterprise move their headquarters out of California and Elon Musk moves to Texas, California is considering raising taxes on the wealthy to unprecedented levels. Experts say California needs to find more ways to reverse the trend.

President Trump declines to say how much he has paid in federal income taxes, Judge Barrett goes under the political microscope, and Walgreens cashier pays for customer’s items with her last $20.

One of the greatest myths for future retirees is that expenses will drop when you retire. Some think their living expenses will virtually cut in half overnight.

However, that is usually not the case. In fact, oftentimes retirees spend more in retirement (especially in the first few years) than they did during their working days. Why is that?

Myth #2 – Social Security Will Provide for Most of My Retirement Needs

Many people are led to believe that they’ll manage to live just on Social Security in retirement. In most cases, however, that’s just not doable. Today, Social Security pays the average recipient only $1,461 a month in benefits. Over the course of a year, that’s $17,532. Meanwhile, the average retired household spends $46,000 a year. So there is a pretty large disconnect between the two. Property taxes alone in some blue states amount to what some receive all year in Social Security payments.

Myth #3 – I Can Just Keep Working

Surveys show that many people nearing retirement would prefer to continue working to close any gaps they feel they have in their retirement funding. Or they want to continue working because they have no plans for their free time after they retire. Regardless of which reason, they want to keep working- and it does provide a dual benefit- it gives a further boost to your nest egg while at the same time reduces the number of years you’ll need to live off it.

Myth #4 – It’s Too Late To Start Saving

They say the eighth wonder of the world is compound interest. And it obviously has a bigger effect the earlier you start saving, but you’re never too old to take advantage of its power to grow your money.

Aside from compounding, the IRS gives other incentives to save for those nearing retirement. IRAs, 401Ks, and other tax-advantaged plans give investors that are 50 and older the ability to make ‘catch up’ contributions. Those Traditional and Roth IRAs can make an additional $1,000 each year per investor. 401Ks and like plans can add $6,000 as a catch-up.

Myth #5 – Taxes Will Be Much Less In Retirement

As you’ve seen in previous points, where we show your need to save more, invest more, and possibly work more – you will probably not be reducing your overall income that much. So if your income isn’t going to drop, then you shouldn’t assume with any honesty that your tax bill will drop.

The Trump tax cut reduced rates, but removed certain deductions. Even if we call it a wash, not many would bet that rates would drop further from here. The easy bet would be to wager they will only rise from here.